2020.09.21

Industry News - 2020.09.21

1、百件起訂・7日起貨・顛覆服裝業 阿里巴巴建「犀牛工廠」助中小企轉型

阿里巴巴旗下工廠再添新成員,針對服裝業設立的「犀牛工廠」,可縮短服裝製造時間,由平均 1,000 件起訂、15 日交付的流程,縮短為 100 件起訂、7日交貨,以小單量、多批次方式,顛覆服裝業生態,中小型服裝品牌亦因為廠家快起貨兼可小批量生產,業務發展處理更靈活。

時間・起訂數量減少 為中小企提供新選擇

阿里巴巴透露,「犀牛工廠」透過自家平台上分析消費行為,為淘寶、天貓商家提供時尚趨勢預測。此外,借助阿里巴巴數碼方案能力,改革傳統服裝供應鏈,將行業平均 1,000 件起訂、15 日交付的流程,縮短為 100 件起訂、7 日交貨,為中小企業提供小單量、多批次、高品質的生產選擇。

「犀牛工廠」與傳統製造工廠不同,前者應用了不少科技元素,如產前排位、生產排期、吊掛路線,都可以由 AI(人工智能)機器做決策。犀牛工廠亦配備「智慧大腦」,以犀牛數碼設計系統聯動需求和供給兩側,可 3D 快速仿真測試、為商家提供基本報價、為供應鏈提供採購數據、為生產提供工藝指導,可加速產品上新、換款。

犀牛工廠表示,每塊布料都有獨立的 ID,由進廠、裁剪、縫製、出廠可以追蹤、自動出入庫存管理、自動配送和智慧化挑選,資源利用率較行業平均提升 4 倍。

除了科技應用,廠房亦使用環保洗水技術,透過 E-Flow 霧化技術,代替傳統洗水處理,每件衣服的用水量可比傳統洗水減少 1/3 ,大大減低排放量,提升洗水技術競爭力。

資料來源:香港經濟日報 (2020年9月18日)

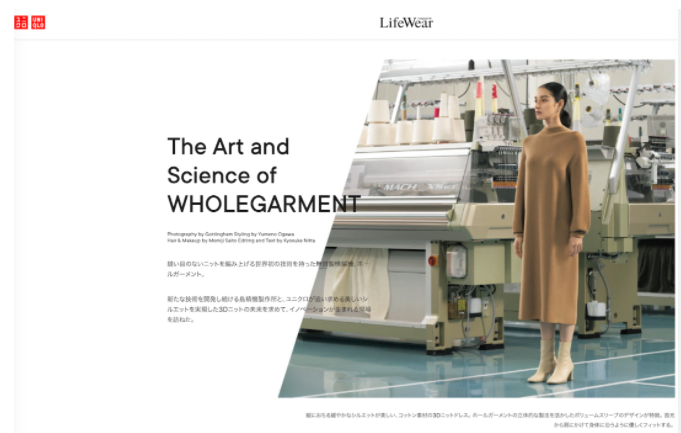

2、優衣庫母公司迅銷集團控股與島精機制作所的合資企業

日前,日本快時尚巨頭優衣庫(Uniqlo)母公司迅銷集團(Fast Retailing)宣佈,成為合資公司 Innovation Factory 的控股方。後者是一家原本由日本針織設備巨頭 —— 島精機制作所於2015年12月創立的全資子公司,專門用於生產 Wholegarment 無縫針織產品。

交易完成後,迅銷集團將持有 Innovation Factory 51%的股權,島精機制作所繼續持有49%股權。

2016年10月,Innovation Factory 轉為合資公司模式,迅銷集團和島精機制作共同出資4億日元,基於 Wholegarment 針織技術,確立全新的生產體系,共同開發和生產針織產品。當時合資公司的股權結構為:迅銷集團持股49%,島精機制作所持股51%。

2017年,迅銷集團在紐約發佈了無縫立體針織技術 3D U-Knit,該技術基於 Wholegarment 技術進一步研發,最大的特點是沒有縫線的立體編織。

迅銷集團表示,本次收購 Innovation Factory 的控股權,會將該公司遷址至迅銷總部——有明中心的近郊,並擴大生產規模,新工廠預計於2021年投入使用。迅銷集團未來將進一步加強以 3D針織技術為中心的針織品生產體系,並將技術要點傳授給位於越南、中國等海外市場的合作工廠。

關於島精機制作所(SHIMA SEIKI MFG., LTD.)

1962年創立時,島精機制作所是日本和歌山市一家製造針織橫機的小工廠。從手套橫編機自動化起步,目前業務涵蓋電腦橫機、服裝設計系統、自動裁剪機以及手套、襪子編織機等產品的開發、生產以及銷售。在電腦橫編機領域中佔有率居世界第一位。截止2019年3月的財會年度,島精機制作所的總營業額為 393.52億日元(約合人民幣 25.5億元),員工總數近2000人。

資料來源:www.htt.hk (2020年9月19日)

3、鍾國斌:禁新疆棉 影響超停標香港製造

美國政府日前公布,禁止新疆部分地區出產的棉花、衣服及其他產品輸往美國。在本港,自由黨黨魁鍾國斌周五於電台節目表示,美國有關措施,較禁止香港出口到美國的貨品使用「香港製造」標籤的影響更大。

鍾國斌解釋,中國八成棉花產自新疆,由中國棉花製成的產品可能會被禁止出口到美國,這項新禁令造成很大影響。他建議,按中美貿易協議,中國需採購大量美國農產品,未來可買入更多美國棉用作對沖,以便解決問題。

他預期,本港產品不會被美國加徵現時適用於中國貨品的關稅,加上全球190多個國家中,僅美國提出有關要求,本港出口到其他地方的產品仍然可以標示「香港製造」,整體影響不大。

美國服裝與鞋類商會總裁Stephen Lamar在國會眾議院撥款委員會聽證會上表示,美國因應新疆少數民族被強制勞動,故限制當地棉花進口美國,惟實際上難以執行。

美服裝商會指難查來源地

他指出,新疆棉花佔全球棉花供應的兩成,雖然相關行業已努力查明棉花來源地,但不大可能完全確定是否來自新疆,因為新疆棉花或與美國及其他地方生產的棉花混合使用,同時,越南、印尼等地的服裝製作也可能使用來自新疆的棉花,這些地方實難準確追蹤棉花來源。

資料來源:信報財經 (2020年9月19日)

4、just-style’s online magazine - Material developments

Material developments: New fibre and fabric innovations set to reshape fashion

Issue 07 - September 2020

In this issue: We look at ways in which the industry is responding to the pandemic, and how research has ramped up to develop new technologies that tap into growing demand for antimicrobial, virus and bacteria killing fibres and fabrics.

Source: www.just-style.com (21 Sep 2020)

5、Apparel’s Fixing Everything but its Glaring Inventory Problem

Inventory optimization has always been crucial for apparel retailers, but in the Covid-19 environment, the quest to sell slow-moving and excess inventory becomes even more complicated, as much of the extra merchandise lying in warehouses, distribution centers and stores alike is in danger of becoming obsolete.

Ronen Lazar, CEO and co-founder of Inturn, an enterprise software solution designed to empower brands to efficiently clear out this backed-up inventory through data-driven go-to-market recommendations, noted that the apparel and fashion industry is still reluctant to implement critical back-end technologies. In particular, he said apparel still lags behind other retail and consumer categories as far as adopting the perspective that leveraging data across departments is crucial to making productive decisions.

“Fashion could probably take some good notes from the CPG world, which is a lot more fast-moving and doesn’t have the same seasonal cycles, and with that there’s a real eye on what’s happening and what’s moving,” said Lazar. “Ultimately, with the leveraging of data, I think the fashion industry will be in a far better place.”

This makes digitization a primary challenge that the industry must tackle head on, particularly if there’s any way they want to get out of the pandemic in a positive position. Many of these inventory problems were persistent well before the pandemic spread, with Lazar noting that some clients actually saw 50 percent increases in slow-moving and obsolete inventory year-over-year in 2019. This is because much of the innovation in retail, unfortunately, has taken place in consumer-facing technology, instead of the back office.

“Now Covid hits, and for fashion folks, you have an environment where stores shut down, goods were in transit from different parts of the world and literally showed up at companies’ doorsteps. What do they do with that? Those who were heavily reliant on brick-and-mortar and wholesale like department stores, they were cancelling orders so that created a lot of supply-chain disruption. Ultimately, there’s an oversupply and a mismatch on seasons. The time value of the goods didn’t present itself for an opportunity to just sell them.”

The expected high level of promotional activity in the upcoming season makes markdown optimization even more important, particularly since consumers at this point are entering the transaction expecting a discount. While markdowns might seem to be inevitable, apparel retailers now are tasked with being able to rescue margin on product before it is too late to sell it.”

“It’s a really tough environment in a sense that you have brand integrity to be concerned about,” Lazar said. “You have your plan that you’re trying to hit, but when you don’t see enough demand in the market, it becomes this chain effect where you have this promotional environment that has existed all this time and continues to gain steam. With the right level of promotional markdown and sales opportunity, I think we could see an interesting holiday season in terms of volume purchase, but the requirement to actually get that will require significant markdowns of product.”

Historically, inventory management processes are manual, tedious and time consuming, with product data often plugged into and pulled from spreadsheets. This data wasn’t as transparent from a cross-functionality perspective, as users could sometimes scrub data they weren’t interested in sharing with other teams, so financial, planning, sales and other departments might determine what products they want to sell at a discount without all the relevant data points.

Where Inturn steps in is by centralizing visibility and enabling real-time collaboration across brands, teams, departments and geographies so all parties can see what inventory needs to be moved, where it is it sitting and what strategies are necessary to take it to market.

“This capitalizes on inventory that otherwise is going to have to be destroyed or it’s going to have to be donated, that’s going to lose tremendous value in the process,” Lazar said. “It’s designed to move that process upstream and open your eyes effectively 60 days earlier, and collaborate so you can engage with the market and determine what is most productive on margin, and what prices protect the brand so you’re not setting yourself up for a channel conflict.”

The company claims its solution can bring drastic changes to the timing of an end-to-end product journey, with clients decreasing their go-to-market time by up to 60 days and shortening average transaction time by 55 percent. Additionally, Inturn says it can reduce operating expenses by 85 percent and increase margin recovery by more than 10 percent.

Inturn recently reported that its enterprise software solution is now an SAP Endorsed App, available through the SAP App Center. With the endorsement, the solution will be more entrenched in the SAP cloud infrastructure, enabling data to flow more quickly and easily across different systems, Lazar said.

“At the onset, pulling the master data is key to being able to react on the fly,” he added. “The truth is, it’s not even to react, it’s to be proactive about what precisely you are sitting on today that could be classified as slow-moving or excess at the snap of a finger, so to speak.”

Source: www.sourcingjournal.com (18 Sep 2020)

6、McKinsey: This is When US Apparel Sales Will Return to Pre-Covid Levels

With Covid-19 cases hitting record levels in the Midwest, uncertainty looming over the timing of a potential vaccine, the dearth of rapid testing and no clear prognosis for when the pandemic might functionally end, don’t expect U.S. retail to rebound to pre-crisis levels anytime soon, cautioned a leading management consulting firm on Wednesday.

Despite the boost from e-commerce, North American apparel sales are poised to fall 20 percent to 30 percent from 2019 levels in 2020 and 10 percent to 25 percent from 2019 levels in 2021, McKinsey & Company analysts said in virtual briefing.

Althea Peng, who leads McKinsey’s apparel, fashion and luxury practice for the Americas, says she’s hopeful for a bullish scenario, where foot traffic might return to stores in the second quarter of 2021. But a bearish scenario, characterized by a wave of virus insurgencies, additional foreclosures, limited stimulus impact, low vaccine adoption and higher consumer pessimism, could keep shopping malls looking like ghost towns till the first quarter of 2022.

The earliest apparel sales might return to pre-pandemic levels, she added, is Q1 2023. If dire conditions persist through next year, retailers can expect to languish till Q2 2025.

Online sales, Peng said, will continue to gain market share, though they won’t be enough to compensate for the decline in brick and mortar. “In 2019, we were roughly 80 percent brick and mortar and 20 percent online,” she said. “This is projected to shift to more of a one-third/two-thirds split between online and brick and mortar in 2020.”

E-commerce penetration is expected to come down just slightly in 2021 as stores are expected to be mostly open for the full year, in contrast to the mass closures that defined most of 2020 and resulted in several retailers, including iconic businesses such as Century 21 boarding up for good, and others like Lord & Taylor heading for a six-foot-under fate. The absolute increase in e-commerce sales from 2019 to 2021 (a compound annual growth rate of 16 percent) will be mostly offset by lower brick-and-mortar sales (a -15 percent CAGR drop).

Not all channels will perform the same, however. Digital-first brands and retailers are doing better than ever, gaining an extra 20 percent in sales from 2019 levels in 2020 and a projected 25 percent from 2019 levels in 2021. “Amazon and other digital-first retailers have been able to do not only rapid recovery but [achieve] real gains during this period as consumers have moved their [dollars] online,” Peng said.

Mass retailers—think Target and Walmart, both of which posted record second-quarter sales—have also overperformed, not only because of their one-stop-shop upper hand but also because they’ve been able to remain open during stay-at-home orders.

One sector that has seen one of the biggest slumps is off-price retailers, which saw sales tumble 40 percent from 2019 levels this year because of their reliance on physical transactions and low e-commerce penetration. They may be able to make a more rapid recovery, with an anticipated 20 percent drop from 2019 levels in 2021, though this is predicated on a return of store traffic.

Vertically integrated brands and department stores, Peng said, are also floundering, sliding 40 percent from 2019 levels in 2020 with a mere 5 percent improvement expected in 2021.

Emma Spagnuolo, a McKinsey associate partner, anticipates some customers’ use of online channels to stick even after the contagion is no longer a threat. According to a recent poll, consumers’ willingness to buy clothing and footwear online post-pandemic jumped 8 percent to 10 percent points. “So this means we have net newbies, who before had not been making any purchases online, now will be moving at least some of their digital purchases to the digital channel,” she said.

Adding to the “complexity” is the fact that she’s seeing a 35 percent to 40 percent growth in users of omnichannel-type services—such as buy online, pick up in store and purchasing through social media or apps—post-Covid-19. (The only behavior not expected to linger past the pandemic, Spagnuolo said, is curbside pickup.)

All of this presents a double-edged sword. Coupled with the inefficiencies of legacy operating models, high shipping and logistics fees that cannot be passed onto the consumer, higher return rates, the steeper cost of acquisition at scale in digital, a shift to e-commerce will likely put the squeeze on profitability.

Successful retailers, Spagnuolo said, approach e-commerce from two angles: capturing a greater share of traffic by boosting conversion and retaining customers, and “supercharging profitability” by thinking outside the traditional legacy model to find ways to reduce costs across the system, increase data transparency and promote the proper attribution of costs to create clarity and accountability.

On the revenue side, the winners are the ones who put the customer at the forefront, chiefly through personalization. “A seamless experience on your website will [also] allow them to go to your website more often and make them more comfortable shopping your site,” she said.

Source: www.sourcingjournal.com (18 Sep 2020)